Quick Takes

- Strong Stock Markets. As in August, the stock market declined before returning to positive territory to close out September. The first week of September saw the S&P 500 decline by over 4% and the Nasdaq decline nearly 6%. Both indices ended the month higher finishing up over 2% each.

- Inflation and Interest Rates. The FOMC cut interest rates in September by 50 bps, which boosted stock and bond markets. Core CPI inflation stood at 3.2% in the month while the Fed’s preferred metric, the PCE Index, indicated that inflation has now fallen to just 2.2%. Thus, more rate cuts are probably ahead.

- Geopolitics. The Middle East will be key to watch in October after Iran launched missiles at Israel in late September as Israel fights a war in Gaza against Hamas and in Lebanon against Hezbollah. This conflict could make the near-term less certain for markets given the importance of the region for global energy supply.

- Hurricane Helene. The tropical storm hit the Southeastern US hard at the end of the month, particularly Florida, Georgia, and the Carolinas. The storm destroyed entire communities and caused billions of dollars worth of damage that will likely take years to repair.

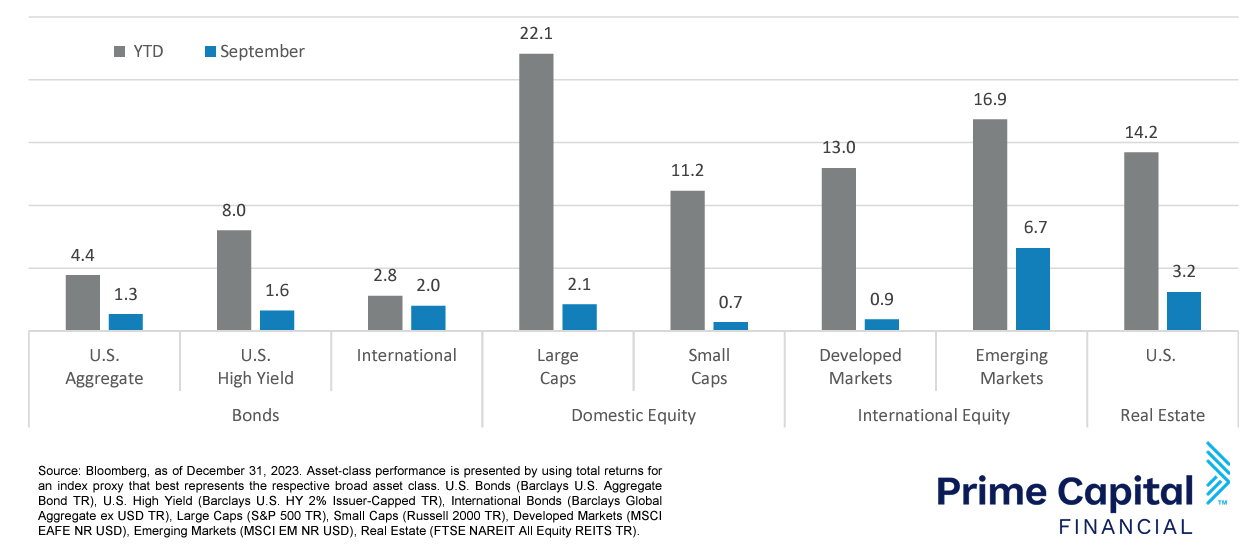

Asset Class Performance

Large Caps had a strong September relative to Small Caps, continuing August’s pattern. International equities underperformed the U.S. market during the month amid conflict in the Middle East and changes in monetary policy. Asset classes across the board saw gains in the month of September including both fixed-income and equities.

Markets & Macroeconomics

On September 18, Federal Reserve Chairman Jerome Powell announced that the FOMC had reduced the Fed’s policy rate by a half percentage point, or 50 bps. This was a larger cut than had been expected earlier in the month by investors. The stock market rallied on this news as well as on Powell’s strong indication that the Fed would continue to loosen policy gradually thanks to the falling rate of inflation that the US has experienced over the last 24 months. The US Core CPI was just 3.2% higher than it was a year ago compared to the peak YoY increase of 6.5% in September of 2022. Meanwhile, the labor market has weakened. Monthly job creation has slowed from well over 200,000 jobs per month to 159,000 in August. Unemployment has risen year to date from 3.7% to 4.2%. In addition to highlighting the progress made on inflation, Powell also highlighted the need to prevent further slowing of the economy or loosening of the labor market. The S&P 500 was up over 2% in September after it recovered from an early decline in the index in the first half of the month. The technology-heavy Nasdaq was up 2.5% in September largely in response to the interest rate reduction. Stock market valuations remain above historical averages as investors remain optimistic about the economy and company results. By the end of September, the S&P 500 was up 21% year to date while the Nasdaq was up 19%. October will be a busy month for earnings releases by companies with major banks and health care companies reporting earnings at the beginning of the month and larger technology, communication services, and consumer companies reporting their results at the end of the month. These reports will be critical in assessing the market outlook for the rest of 2024 and into the beginning of 2025. They will also be essential for assessing if the Federal Reserve has managed to achieve a soft landing. It will also be critical to see how the presidential candidates will talk about their plans for the economy going into the November election and how geopolitical events will impact markets given the conflict in the Middle East. China will also be worth watching as the central bank tries to boost economic growth.

Bottom Line: Easing inflation and loosening monetary policy made investors more optimistic in September. More FOMC interest rate cuts are probable going forward if inflation continues to fall and remain at the long-term target rate of 2%. Weakness in the labor market was a remaining risk at the end of September which could indicate that a slowdown is ahead. The next month of economic releases and new earnings data will be a useful gauge of how well the economy and companies are faring relative to investors’ lofty expectations.

Download the full review.

©2024 Prime Capital Investment Advisors, LLC. The views and information contained herein are (1) for informational purposes only, (2) are not to be taken as a recommendation to buy or sell any investment, and (3) should not be construed or acted upon as individualized investment advice. The information contained herein was obtained from sources we believe to be reliable but is not guaranteed as to its accuracy or completeness. Investing involves risk. Investors should be prepared to bear loss, including total loss of principal. Diversification does not guarantee investment returns and does not eliminate the risk of loss. Past performance is no guarantee of comparable future results.

Source: Sources for this market commentary derived from Bloomberg. Asset‐class performance is presented by using market returns from an exchange‐traded fund (ETF) proxy that best represents its respective broad asset class. Returns shown are net of fund fees for and do not necessarily represent performance of specific mutual funds and/or exchange-traded funds recommended by the Prime Capital Investment Advisors. The performance of those funds June be substantially different than the performance of the broad asset classes and to proxy ETFs represented here. U.S. Bonds (iShares Core U.S. Aggregate Bond ETF); High‐Yield Bond (iShares iBoxx $ High Yield Corporate Bond ETF); Intl Bonds (SPDR® Bloomberg Barclays International Corporate Bond ETF); Large Growth (iShares Russell 1000 Growth ETF); Large Value (iShares Russell 1000 Value ETF); Mid Growth (iShares Russell Mid-Cap Growth ETF); Mid Value (iShares Russell Mid-Cap Value ETF); Small Growth (iShares Russell 2000 Growth ETF); Small Value (iShares Russell 2000 Value ETF); Intl Equity (iShares MSCI EAFE ETF); Emg Markets (iShares MSCI Emerging Markets ETF); and Real Estate (iShares U.S. Real Estate ETF). The return displayed as “Allocation” is a weighted average of the ETF proxies shown as represented by: 30% U.S. Bonds, 5% International Bonds, 5% High Yield Bonds, 10% Large Growth, 10% Large Value, 4% Mid Growth, 4% Mid Value, 2% Small Growth, 2% Small Value, 18% International Stock, 7% Emerging Markets, 3% Real Estate.

Advisory products and services offered by Investment Adviser Representatives through Prime Capital Investment Advisors, LLC (“PCIA”), a federally registered investment adviser. PCIA: 6201 College Blvd., Suite#150, Overland Park, KS 66211. PCIA doing business as Prime Capital Financial | Wealth | Retirement | Wellness. Securities offered by Registered Representatives through Private Client Services. Member FINRA/SIPC.

© 2024 Prime Capital Financial, 6201 College Blvd., Suite #150, Overland Park, KS 66211.