Quick Takes

- Stocks Higher. U.S. equity indices were higher in May as temporary breaks on tariffs and relatively strong earnings boosted sentiment. The S&P 500 jumped 6.1% and the Nasdaq 100 rose 9.0%. The Magnificent 7 rose about 13.3% in May as big technology companies reported quarterly results.

- Inflation and Interest Rates. The 10Y treasury yield rose in May to 4.4% as the U.S. House passed a budget bill that is expected to increase the deficit. Core PCE inflation for April was 2.5% while headline PCE inflation was below expectations at 2.1% mostly on lower food and energy inflation.

- Trade Negotiations. The U.S. and U.K. agreed to reduce some tariffs on cars and steel after a meeting between U.K. Prime Minister Kier Starmer and President Trump. The U.S. also reached a temporary agreement with China to pause tariffs put in place since April for 90 days and to reduce rates thereafter from the triple-digit levels touted before.

- U.S. Fiscal Policy. The House of Representatives passed a bill to extend the 2017 tax cuts, increase spending on the military and immigration enforcement, and reduce spending on Medicaid, SNAP benefits, and EV and green energy subsidies.

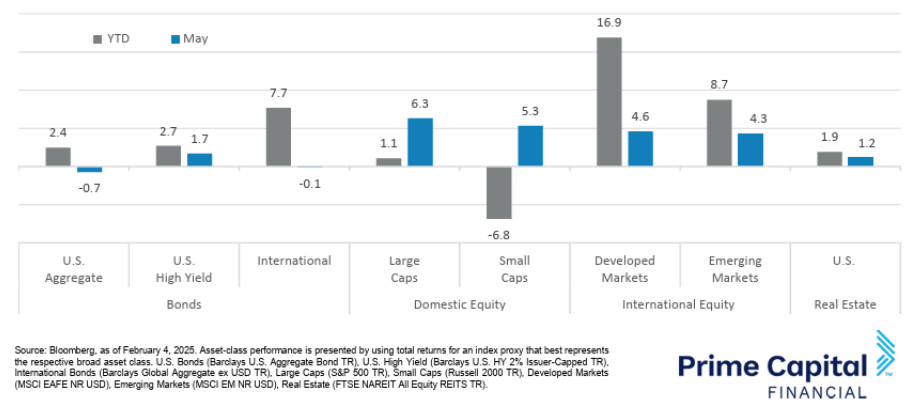

Asset Class Performance

Large caps outperformed small caps in May. U.S. stocks outperformed international stocks for the first time in four months as tariff reprieves and temporary trade agreements, better consumer sentiment, and strong technology earnings boosted U.S. stocks. Stocks and real estate were generally higher in May while U.S. bonds fell.

Markets & Macroeconomics

On May 7, the Fed announced that it was maintaining its policy rate at 4.25%4.50%. Later in the month, the Trump administration reached some temporary agreements on tariffs with major U.S. trade partners including China and the U.K. The agreement with the U.K. involved the U.S. reducing its metals tariffs on aluminum and steel to 0% from 25% and reducing tariffs on imported cars from the U.K. The U.K. in return reduced some tariffs on imports from the U.S. including agricultural products and aerospace components. With China, U.S. officials agreed to a 90-day pause on tariffs that the two countries have put in place since April and a reduction in tariff rates. China agreed to reduce its tariff rate on imports from the U.S. from 125% to 10% and the Trump administration agreed to reduce U.S. tariff rates on imports from China from 145% to 30%. JP Morgan and Goldman Sachs raised GDP growth forecasts for the U.S. and China as a result of the tariff truce. Restrictions on exports of advanced semiconductors still remain in place and were even expanded in May by the Trump administration. The agreements with the U.K. and China helped consumer sentiment improve in May as Conference Board Consumer Confidence rose to 98.0 in May from 85.7 in April. Retail sales growth slowed considerably in April as consumers cut back on spending after increasing it sharply in March in anticipation of tariffs. In the labor market, the U.S. added 177K jobs in April and the unemployment rate remained steady at 4.2%. The March jobs growth number was revised down from an addition of 228K jobs to just 185K new jobs. The labor force participation rate also increased slightly from 62.5% to 62.6% in April. In the housing market, pending home sales fell by 6.3% month-over-month in April, the largest monthly decline since September of 2022 largely on tariff announcements and persistently high mortgage rates. Headline inflation, as measured by both PCE and CPI fell in April as lower oil and food prices helped ease price pressures. Headline CPI fell to 2.3% from 2.4% in March and headline PCE fell from 2.3% to 2.1%. Core CPI inflation remained steady at 2.8% in April while core PCE inflation fell from 2.6% to 2.5%.

Bottom Line: Job growth remained strong in April while consumer sentiment improved on temporary trade policy easing, but uncertainty remains in the economy around how trade policy and negotiations with trade partners will impact the economy moving forward.

©2025 Prime Capital Investment Advisors, LLC. The views and information contained herein are (1) for informational purposes only, (2) are not to be taken as a recommendation to buy or sell any investment, and (3) should not be construed or acted upon as individualized investment advice. The information contained herein was obtained from sources we believe to be reliable but is not guaranteed as to its accuracy or completeness. Investing involves risk. Investors should be prepared to bear loss, including total loss of principal. Diversification does not guarantee investment returns and does not eliminate the risk of loss. Past performance is no guarantee of comparable future results.

Source: Sources for this market commentary derived from Bloomberg. Asset‐class performance is presented by using market returns from an exchange‐traded fund (ETF) proxy that best represents its respective broad asset class. Returns shown are net of fund fees for and do not necessarily represent performance of specific mutual funds and/or exchange-traded funds recommended by the Prime Capital Investment Advisors. The performance of those funds June be substantially different than the performance of the broad asset classes and to proxy ETFs represented here. U.S. Bonds (iShares Core U.S. Aggregate Bond ETF); High‐Yield Bond (iShares iBoxx $ High Yield Corporate Bond ETF); Intl Bonds (SPDR® Bloomberg Barclays International Corporate Bond ETF); Large Growth (iShares Russell 1000 Growth ETF); Large Value (iShares Russell 1000 Value ETF); Mid Growth (iShares Russell Mid-Cap Growth ETF); Mid Value (iShares Russell Mid-Cap Value ETF); Small Growth (iShares Russell 2000 Growth ETF); Small Value (iShares Russell 2000 Value ETF); Intl Equity (iShares MSCI EAFE ETF); Emg Markets (iShares MSCI Emerging Markets ETF); and Real Estate (iShares U.S. Real Estate ETF). The return displayed as “Allocation” is a weighted average of the ETF proxies shown as represented by: 30% U.S. Bonds, 5% International Bonds, 5% High Yield Bonds, 10% Large Growth, 10% Large Value, 4% Mid Growth, 4% Mid Value, 2% Small Growth, 2% Small Value, 18% International Stock, 7% Emerging Markets, 3% Real Estate.

Advisory products and services offered by Investment Adviser Representatives through Prime Capital Investment Advisors, LLC (“PCIA”), a federally registered investment adviser. PCIA: 6201 College Blvd., Suite#150, Overland Park, KS 66211. PCIA doing business as Prime Capital Wealth Management (“PCWM”) and Qualified Plan Advisors (“QPA”). Securities offered by Registered Representatives through Private Client Services, Member FINRA/SIPC. PCIA and Private Client Services are separate entities and are not affiliated.

© 2025 Prime Capital Investment Advisors, 6201 College Blvd., Suite #150, Overland Park, KS 66211.